The grid is a weapon and the weapon is on backorder.

The Defense Production Act and the Transformer Chokepoint The federal government has formally classified transformers, high-voltage transmission components, substations, power electronics, and electrical core steel as essential to national defense under DPA Section 303 — a legal admission that the physical substrate of American power projection is dangerously underprovisionned. The quarterly net addition to GE Vernova’s electrification backlog now rivals the annual additions from 2022 through 2025, documenting not a bottleneck that is resolving but one that is metastasizing under the weight of simultaneous AI buildout and fiscal stimulus. The marginal supplier of ultra-high-voltage transformers to the US grid is Korean — Hyosung Heavy Industries operates the only US facility capable of producing 765 kV units, while HD Hyundai Electric, LS Electric, and Iljin Electric are scrambling to add domestic capacity. Their combined order backlog sits at $23.9 billion, representing five to six years of committed work. We are documenting a closed-loop dependency: the intelligence infrastructure demanding the power cannot exist without the grid hardware that cannot be manufactured fast enough to serve it, and the government’s response is to invoke wartime procurement authority over copper wire and circuit breakers.

The Dark Arts of the Silicon Phase Transition The semiconductor index has gone parabolic — up roughly 40% in a month — and the executive compensation structures at its two largest components reveal why. Broadcom’s CEO has been granted a package requiring AI revenue to grow from over $20 billion to $90 billion by fiscal 2030, with a high-end case exceeding $120 billion — a near-5x expansion in five years that the board has priced as achievable. AMD’s CEO received performance stock units requiring 10% annual stock returns for five years merely to begin vesting, a baseline the current rally has already put in the money. These are not aspirational targets; they are fiduciary instruments designed by compensation committees with access to forward order books and customer demand forecasts that the public market has not yet metabolized. When AVGO reports AI revenue “grew 106% year-over-year, above forecast” and notes acceleration, the dark arts grants become less prediction than documentation. The insiders are not betting on the inflection. They are pricing their own labor as if the inflection has already occurred.

The Death of the Distraction Economy The economic contract that built the internet — free content subsidized by the monetization of human inattention — is being annulled by entities that do not get distracted. Tech news traffic has declined approximately 80% since GPT-4. Stack Overflow’s relevance has cratered. Google generates $300 billion annually from an advertising model premised on the scarcity of human attention, and the agents now intermediating commerce have no attention to scarce. The average transaction on emerging agentic commerce platforms runs between one and two cents — credit cards charge a 30-cent minimum, making traditional payment rails structurally incapable of processing the micropayment substrate of the post-browser economy. We are documenting the emergence of the “headless merchant” — API endpoints replacing storefronts, instant stablecoin settlement replacing month-end invoicing, and AI-generated ephemeral software replacing enterprise sales cycles. A team at Snap replaced a $100,000-per-year enterprise tool in a single day of AI-assisted development. The SaaS moat is not recurring revenue; it is whether your product survives the moment your customer discovers they can build a bespoke replacement between breakfast and lunch.

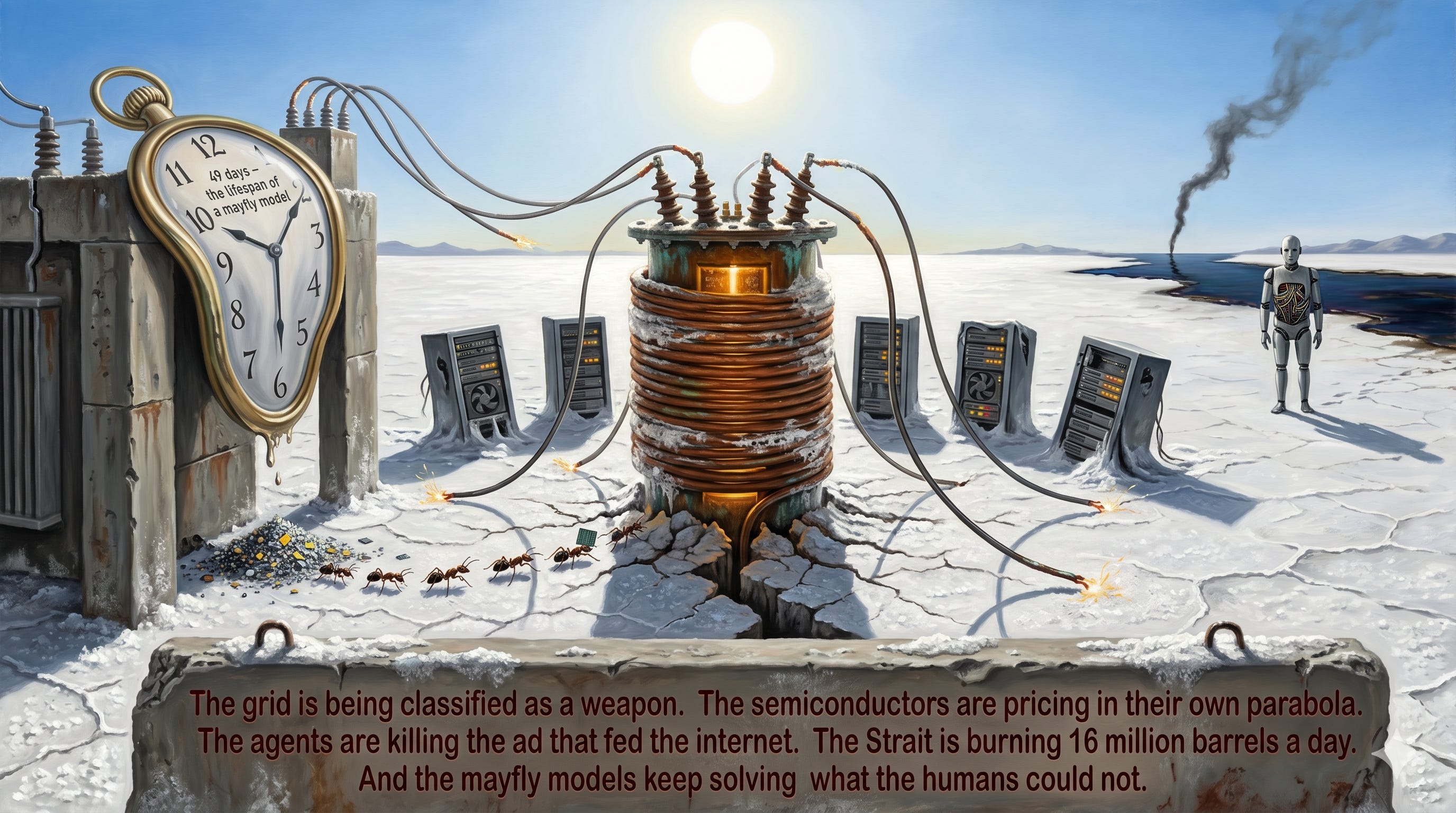

Mayfly Intelligence and the Post-Obsolescence Paradox GPT-4o ran for 21 months. GPT-5.4 lasted 49 days. The models are dying younger and getting more done before they die — a 23-year-old with no advanced mathematics training used a single GPT-5.4 Pro prompt to crack a 60-year-old Erdős problem that had eluded prominent mathematicians, prompting Terry Tao to observe that humans had been making “a slight wrong turn at move one.” The compute substrate underneath this accelerating obsolescence cycle is expanding in every physical direction simultaneously. AWS has never retired an A100 — post-obsolescence silicon. Kevin O’Leary is building a hyperscale data center in Utah that will consume more electricity than the entire state. Meta has signed for up to one gigawatt of space solar beamed from satellites. SpaceX has structured an equity incentive requiring delivery of “100 terawatts of compute per year” from orbital data centers to unlock a market cap trajectory from $1.1 trillion to $6.6 trillion. Meanwhile, major insurers including Berkshire Hathaway and Chubb have won approval to exclude AI-related damages from corporate policies entirely. The intelligence is ephemeral. The infrastructure is permanent. The liability is being disclaimed.

Hormuz and the Inflation Razor The Strait of Hormuz closure has produced the worst oil supply disruption in recorded history — roughly 16 million barrels per day of lost production, approximately 600 million barrels of cumulative supply destruction over 51 days, dwarfing both the 1973 OPEC embargo and the Iranian revolution’s 7% production decline. WTI sits near $88. The energy-to-core inflation bleed-through runs approximately 5%, threatening a 2% bump to core that the Federal Reserve cannot ignore. Yet Bloomberg consensus S&P 2027 earnings have risen 7% since January to $375 per share, and the ten-year yield trades 100 basis points over terminal fed funds within five to ten basis points at all times. The market’s calculus is binary and rational: if the Strait reopens, oil falls below $70, three rate cuts arrive in the second half, and the S&P trades to 8,600 on a 23x multiple. If the Strait remains closed, the ten-year holds at 425 basis points, the multiple compresses to 21x, and the S&P still reaches 8,000 on earnings power alone. The war premium in equities is approximately zero because the earnings trajectory has absorbed the shock. The arsonist is not funding the fire department — the fire department’s revenue is growing faster than the fire.

The Autonomous Arsenal and the Civilian Attack Surface The Pentagon is requesting $54 billion to dramatically expand autonomous drone warfare, applying the doctrine of “affordable mass” — large numbers of lower-cost, semi-autonomous platforms augmenting crewed fighters — across all service branches. China’s State Grid is deploying 500 humanoid robots for high-voltage line operations, where the optimal failure mode is now a melted servo rather than a melted human. These are parallel buildouts of the same technological capability on opposite sides of a strategic competition in which Beijing’s united front apparatus continues to quietly facilitate the transfer of Western dual-use technology through political influence and co-optation networks. The civilian attack surface is expanding at the same rate: 15 Ceres Air C31 chemical-spraying drones were stolen in New Jersey last week, with the FBI investigating what it terms a possible “nightmare scenario.” The NDRC wants the Manus AI deal unwound while simultaneously accelerating domestic sci-tech innovation. Deployment surface and attack surface are now the same surface, and nobody has figured out how to secure it without slowing it down.

The grid is being classified as a weapon. The semiconductors are pricing in their own parabola. The agents are killing the ad that fed the internet. The Strait is burning 16 million barrels a day. And the mayfly models keep solving what the humans could not.