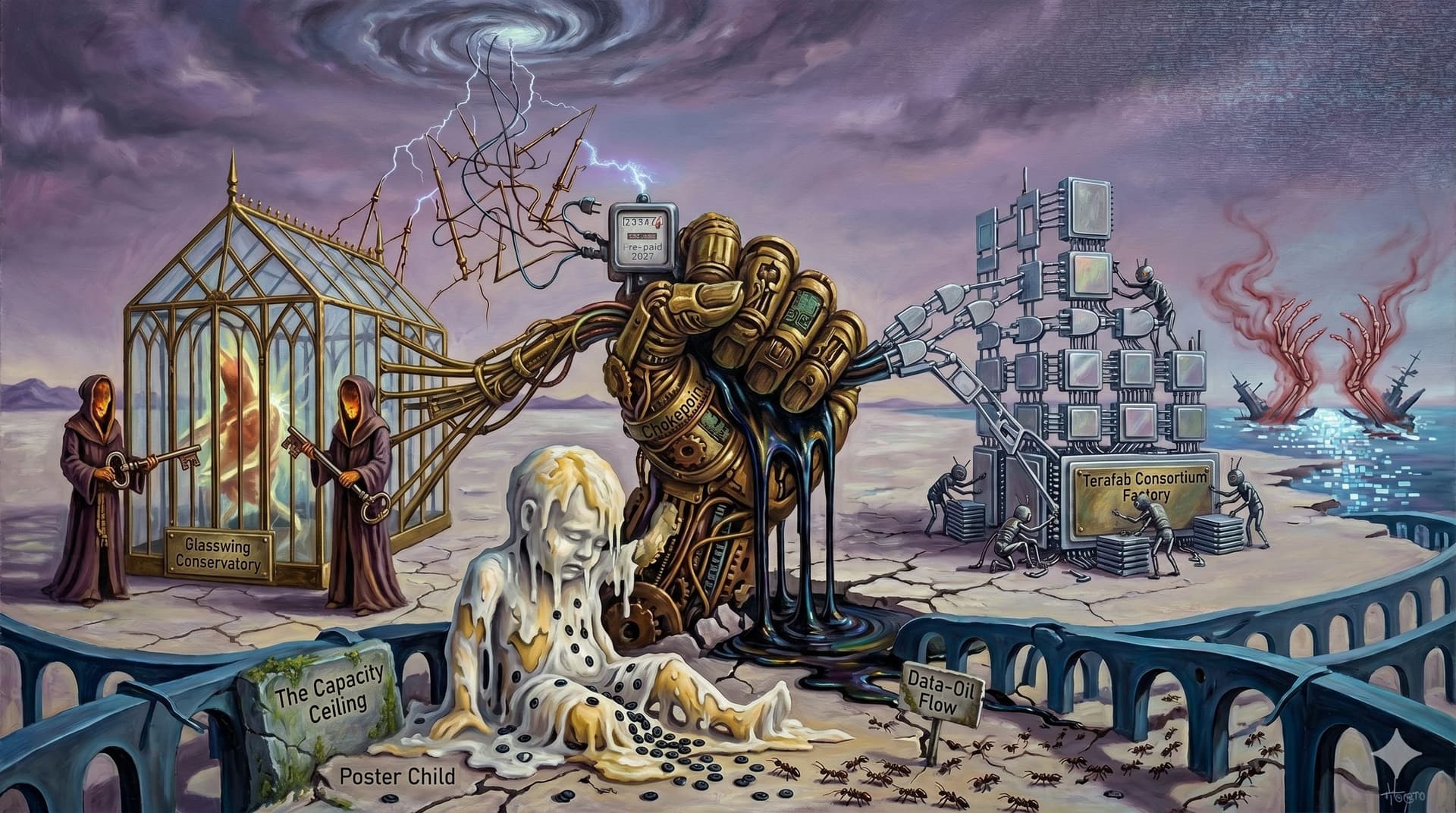

Four coalitions signed documents this week, and the market—bless its simplistic, algorithmic heart—priced them as four distinct headlines. It’s a category error. Project Glasswing isn’t a “safety consortium”; it’s a barricade. When AWS, Apple, Google, and the rest of the TechnoCore huddle in a windowless room to build “guardrails” around a model the public hasn’t seen, they aren’t protecting you. They are protecting the gate.

Anthropic pre-paying for 3.5 gigawatts of power it doesn’t have—power that won’t exist until 2027—is a frantic, adrenalized gamble [v.8.3]. It’s the sound of a man buying all the oxygen in a room before the fire starts. Intel, SpaceX, and xAI forming Terafab to manufacture a terawatt of compute is just more of the same: the realization that the Metabolic Shift is here. We are moving from the era of “software eating the world” to the era of hardware devouring the substrate of reality itself.

[v.8.3] Note: 3.5 gigawatts is roughly three Deloreans’ worth of lightning, or the entire output of the Zaporizhzhia nuclear plant before the geopolitical “unpleasantness.” To buy this much “future” electricity is to admit that the present is already bankrupt.

NATO published a revised Indo-Pacific air defense framework the same week that Iran's asymmetric counterair campaign was shaking two bases in the Gulf. Four treaties in seven days. Written by people who do not usually sign things together.

The question is not whether these four events are connected.

They are the same event, filmed from four angles.

The Big Picture

The Treaty Week: When Former Rivals Sign in the Same Room

The word “coalition” got quiet this week. It stopped being rhetoric and became a legal instrument. Project Glasswing is the clearest version of the pattern — the frontier labs and their biggest customers and their biggest regulators-in-waiting all signing the same page, triggered by a model capability that none of them has publicly seen. The Broadcom–Google–Anthropic TPU agreement for 3.5 gigawatts beginning in 2027 is the same shape with different hats. Terafab is the semiconductor version — chip-hungry companies pooling capital to build a shared substrate because none of them alone can afford to be single-supplier exposed. These are not technology partnerships. They are supply-chain treaties, signed in the knowledge that the alternative is being picked off one at a time. The thing to notice is that the coalitions form before the visible crisis. Glasswing was announced preemptively. The 3.5-gigawatt contract is for power that does not exist. Terafab is a consortium chasing a number — one terawatt — that the participants know none of them can hit individually. Coalitions are leading indicators of scarcity that has not yet been admitted.

The Hormuz Phase II: The War Does Not End When the Ceasefire Does

Fifteen separate strategic-affairs dispatches landed this week on the same desk. Bromine chokepoints. Iran’s anti-access strategy. NATO’s air defense future. The Strait of Hormuz food security implications. French forward deterrence dispersal. Iran’s internet war. Anti-missile gaps in the Indo-Pacific. They read, cumulatively, as one long argument: the ceasefire is a punctuation mark, not a conclusion. The investment thesis underneath the flood is that the defense-industrial base is now being restructured at the tempo of actual conflict, not at the tempo of peacetime procurement. Counter-UAV systems. Domestic interceptor manufacturing. Allied refueling fleets. Strategic bomber and refueler modernization. Each is a small line item. Collectively they are a reshaping of what the defense budget actually buys. The legacy primes are not visibly losing yet. But the capital is flowing in patterns that do not match their revenue maps. Someone is going to be left holding a cost-plus contract for a system that the actual war already made obsolete.

The Poster Child Is on Fire

Microsoft went from fifty-six percent bullish last week to nine percent bullish this week across fourteen independent channels. Nine percent. There is no narrative event that justifies a fifty-point sentiment collapse in seven days. What there is, instead, is an accumulation of small tells finally reaching audible volume — the Copilot buttons being stripped out of Snipping Tool and Photos and Notepad; the enterprise co-pilot fumble becoming the consensus read; Azure’s capacity problem no longer being read as a scarcity bull case and starting to be read as a growth ceiling; the stock printing new lows it has not seen since March 2020. Microsoft is the index for what the broad AI trade looks like when it goes wrong. When the poster child catches fire, the argument is not about one company. The argument is about the thesis the poster child was carrying.

Signal Convergence

The Coalition Layer

The technical journalists, the macro generalists, and the policy strategists converged this week on a single structural observation: the most important deals are not product deals. They are coalition deals. Glasswing is the AI-safety treaty. The 3.5-gigawatt TPU contract is the compute-access treaty. Terafab is the fabrication treaty. The Indo-Pacific air defense framework is the geopolitical treaty. A market that still reads each of these as an isolated catalyst is a market that has not yet priced the fact that the next two years of competitive dynamics will be determined by who is inside which tent. The companies building the interoperability layer — the middleware that makes coalitions technically possible — are being mispriced because the market is still valuing the application layer. The plumbing is where the contracts live.

The Hyperscaler Cash-Flow Pinch

The other converging signal is uglier and harder to argue with. The hyperscalers are spending roughly five times their revenue on AI infrastructure and hoping the story catches up before the balance sheet does. The explicit disclosure this week — that AI capex for Meta, Amazon, Microsoft, Alphabet, Google, and Oracle is on track for $720 billion in 2026, against revenues less than twenty percent of that — is the first time the number has been said aloud in the open. The software ETF, IGV, is down thirty percent year to date. The software names that were supposed to be the AI-beneficiary layer are underperforming the hardware names by a margin that used to be considered impossible. Microsoft is the biggest holder in IGV. The pinch is structural, not cyclical, and the companies that have been absorbing the capex without yet absorbing the revenue are the ones priced for the revenue.

Prediction Markets Get Institutionalized

A smaller signal but a specific one: the infrastructure for prediction markets went institutional this week. Interactive Brokers launched ForecastTrader with the founder of IBKR personally explaining it on two separate podcasts. Kalshi’s signals are appearing in mainstream research. Cathie Wood treated them as real. The thesis is that binary-outcome derivatives are being professionalized — routing, risk management, clearing — at exactly the moment that binary political, macro, and sector outcomes are where the interesting capital wants to express a view. The ticker that concentrates this is IBKR, which this week pulled fifteen mentions across only two explicit channels — a concentration pattern that usually precedes broader coverage.

If this is hitting different, subscribe — next week’s convergence drops Tuesday ->

The Board

The board this week is sourced by function, not by popularity. Eight slots, each filled on a specific mandate rather than raw channel count: two Anchors that actually carry the week’s coalition narrative, three Esoteric names where the coverage is thinner but the mention density or the novelty is the tell, one Divergence pick where the sources openly disagree, one Cross-Domain pick where the convergence cuts across category lines instead of stacking inside one, and one Contrast pick — the name moving the opposite direction from the crowd.

Anchors

AVGO · Stock · 4 sources · 50% bullish (4 bullish / 0 bearish / 4 neutral) · Anchor 3.5 GW Anthropic TPU Deal | Custom Silicon for Hyperscalers | Glasswing Signatory

“Broadcom, Google and Anthropic PBC have expanded their current strategic collaboration under which Anthropic, beginning in 2027, will access through Broadcom approximately 3.5 gigawatts as part of the multiple gigawatts of next generation TPU-based AI compute” — Liberty’s Highlights (quoting the 8-K)

Four sources, 50% bullish, zero bearish — but this is the week’s single most concrete coalition artifact. The Broadcom 8-K disclosing the 3.5-gigawatt multi-year Anthropic deal is not a narrative — it is a legal document. When the disclosure is an SEC filing, the sentiment is documentation, not commentary. AVGO on this board is a load-bearing pick: it reprices a semiconductor conglomerate into a piece of the AI compute treaty system, and it is the one board slot where the catalyst is not subject to re-interpretation next week.

MSFT · Stock · 14 sources · 9% bullish (3 bullish / 8 bearish / 21 neutral) · Anchor Enterprise AI Fumble | Copilot Withdrawal | Azure Capacity Ceiling

“Microsoft I would think the poster child for public companies of the AI trade — new lows back to March 2020. It’s really hard to believe with how much success Microsoft the business has had.” — The Compound

“Microsoft is quietly ripping Copilot buttons out of Snipping Tool, Photos, and Notepad as penance for Windows 11 bloat, proving novelty-phase UX can’t survive the utility phase.” — The Innermost Loop

Fourteen sources, nine percent bullish, eight explicit bearish voices. The largest weekly sentiment reversal we have ever recorded for a mega-cap — 56% bullish last week, 9% bullish this week. MSFT is an Anchor not because it got the most mentions (it did not), but because the coalition week has an obvious counter-story: the mega-cap nobody is signing anything with. When fourteen independent analysts look at the same company and only three can muster a bull case, the poster child is carrying the entire AI-thesis-is-breaking argument on its back.

Esoteric

IBKR · Stock · 2 sources · 15 mentions · 33% bullish (5 bullish / 0 bearish / 10 neutral) · Esoteric — mention-density outlier ForecastTrader Launch | Prediction Market Institutionalization | Peterffy Interview

“IBKR of the brokerage platforms that a retailish person could access, always been one of the most sophisticated in terms of the wide range of instruments that are available from stocks to bonds to futures, etc.” — Odd Lots

“If you go to Interactive Brokers today, there is something we call Probability Lab where we display the probability distribution associated with the future price changes of any stock.” — Odd Lots (Tomas Peterffy)

Two channels, fifteen mentions — the highest mention-density ticker in the candidate pool. Prior 4-week channel count: zero. This is a ticker that arrived on the radar this week via one deep Odd Lots interview with Tomas Peterffy, plus follow-on treatment. The signal is not convergence — it is saturation within a single high-signal channel. ForecastTrader is the thesis: Interactive Brokers is building the prediction-market infrastructure that lets binary political, macro, and sector outcomes trade on a real exchange spine. When a brokerage founder spends an hour explaining why the derivative people should care about forecast markets, the category is being institutionalized in real time.

CSCO · Stock · 2 sources · 0% bullish (0 bullish / 0 bearish / 3 neutral) · Esoteric — novelty Glasswing Signatory | Acceleration from Zero | Coalition-Return Story

“Project Glasswing was created. We’re announcing Project Glasswing, a new initiative that brings together Amazon Web Services, Anthropic, Apple, Broadcom, Cisco, CrowdStrike, Google, JP Morgan Chase...” — Jordi Visser

Cisco has not appeared on this board’s convergence candidates at all in the last 28 days. Then a coalition week happens and it shows up as a Glasswing signatory. No bull or bear sentiment yet — the sources are just naming it as present in the room. That is the signal. Cisco is the name that the market has spent five years pricing as an ex-growth networking company; being inside Glasswing alongside AWS, Anthropic, and JPMorgan is a repositioning event that the sentiment data has not yet caught up to. Esoteric pick, low-conviction sentiment, high-conviction inclusion.

RKLB · Stock · 2 sources · 25% bullish (1 bullish / 0 bearish / 3 neutral) · Esoteric — small-cap, acceleration 2.0x Space Launch Competition | Defense-Software Inflection | Aggressive Multiples

“A lot of the space stocks — Rock Labs, Lunar, that whole bucket — they are trading at pretty aggressive multiples.” — Basis Points

“For launch services, their main competitor is Rocket Lab, which is listed ticker symbol RKLB.” — AdamKhoo (on Starshield)

Rocket Lab is the small-cap version of the defense-software inflection thesis. The Starshield competitor framing (AdamKhoo) and the “aggressive multiples” caveat (Basis Points) are the bull and skeptic voices respectively — not yet a debate, but a live thesis. RKLB is on the board as the illustration of what “the defense primes are structurally incapable” actually buys you if you want to express the trade: the pure-play small-cap that is competing with SpaceX’s national-security launch monopoly.

Divergence

PLTR · Stock · 4 sources · 29% bullish (2 bullish / 4 bearish / 1 neutral) · Divergence — most-split sentiment on the board Growth Rate vs Valuation Debate | Government AI Anchor | Down-Day Tape

“Everybody thought I was crazy when I was saying, listen, Palantir at 100 feels expensive. When you look at all the actual valuations where it’s trading at 200...” — Basis Points “Palantir over the next several quarters is going to have revenue growth deceleration.” — Jeremy Lefebvre Financial Education

Four channels. Two bullish, four bearish, one neutral — and notably, one of the same analysts appears on both sides of the debate in the same week. Palantir is the most-divided sentiment ticker on the board. The split is structural: the growth-rate bulls and the valuation bears are looking at the same income statement and arriving at different conclusions because the question is whether the government AI anchor is durable enough to justify the multiple. The divergence is the trade.

Cross-Domain

INTC · Stock · 8 sources · 38% bullish (3 bullish / 0 bearish / 5 neutral) · Cross-Domain — 8 distinct channel categories Terafab Consortium | Apollo Spinoff | Fab-Plus-Design Integration

“Intel joining Terafab alongside SpaceX, xAI, and Tesla to chase 1 TW/year of compute.” — The Innermost Loop “You should buy Intel. Well, okay, he’s partnering still, maybe might buy it. So Intel says its ability to design, fabricate, and package chips makes Terafab actually work.” — peterdiamandis

Eight channels spanning eight distinct categories — the highest domain-diversity score in the candidate pool. Intel is not the best-performing name, not the highest-conviction name, and not the most-mentioned name — but it is the only ticker this week covered by a macro newsletter, a technical engineering blog, a futurism channel, a substack, a finance vlog, and an interview podcast simultaneously. Cross-domain convergence is a leading indicator: when a ticker is being discussed by analysts who do not share reading lists, the story is real enough to have punched through category walls. Terafab is the Trojan horse; the fab-plus-design integration is the underlying thesis.

Contrast

AMD · Stock · 3 sources · 80% bullish (4 bullish / 0 bearish / 1 neutral) · Contrast — low coverage, highest conviction 450-Series Summer Ramp | Incumbent-Distracted Trade | Benchmark Outperformance

“AMD has gone up almost 11% while the S&P 500 is down 3 and a half percent. AMD is showing major outperformance. 450 series really goes into mass ramp over the summer.” — Jeremy Lefebvre Financial Education

“Looking at shares of Advanced Micro Devices, AMD here — nobody believed it could compete with Nvidia.” — Bowtie Nation

Three channels, 80% bullish, zero bearish — the highest-conviction positive read on the board. AMD is not a coalition name, not a hyperscaler capex beneficiary, not a Mag-7 constituent. It is the second-place chip company outperforming its benchmark by fourteen points on the week while the mega-cap complex rolls over. The 450-series ramp is the concrete mechanism. The trade works if the challenger can take share while the incumbent is distracted by a coalition meeting.

Bear Watch

Bear ORCL · 6 sources · 0% bullish (0 bullish / 2 bearish / 7 neutral)

“Oracle is on track to spend 720 billion on AI infrastructure in 2026 alone, which is less than 20% of the revenue that they’re making.” — The Diary of a CEO

Six sources, zero bullish, two explicit bear voices. Oracle is the clean read on the hyperscaler cash-flow pinch — the capex-to-revenue ratio is now specific enough to be an argument rather than a vibe. When a mega-cap gets six channels of coverage with zero bullish sentiment, that is not neutral. That is a sector-level concern wearing a single ticker.

Bear IGV · ETF · 4 sources · 0% bullish (0 bullish / 4 bearish / 1 neutral)

“look at the IGV stock index down 30% year to date down 5% today all software stocks plummeting” — All-In Podcast

The software-sector proxy, down thirty percent year to date, with four explicit bear voices and no one willing to call a bottom. Microsoft is IGV’s largest holding — which makes IGV the diversified version of the MSFT bear thesis. If the software capex story breaks, this is where it shows up first.

Momentum Watch

Mag-7 coverage without conviction (the “on the radar but not on the board” names): GOOGL (18 channels, 30% bull — widest coverage, lowest conviction), META (16 channels, 34% bull), NVDA (15 channels, 42% bull, 0 bearish — structural scarcity intact), AMZN (13 channels, 46% bull — Trainium valuation disclosure is the specific signal), AAPL (9 channels, 50% bull), BTC (10 channels, 63% bull — digital scarcity thesis re-opening). These are the names the market has to have an opinion about; broad coverage alone is not a thesis.

Accelerating from zero (names with no prior-four-week coverage that surfaced this week): CSCO (Glasswing signatory, on board), IBKR (ForecastTrader, on board). Watch for a third next week.

Highest cross-domain scores (coverage spanning unusually many channel categories): GOOGL (12), META (13), NVDA (10), INTC (8 — on board), MSFT (9), AMZN (9). Cross-domain for the mega-caps is expected; what is notable is INTC at 8 given it only has 8 channels — one category per channel, the purest cross-domain signal in the pool.

Cooling off: GS (-2), MU (-2, after last week’s bull/bear debate), BX (-2), T (-2), TSLA (-4 from last week — the rare Mag-7 losing channels). The banks-and-rates trade is losing channels. The coalition trade is gaining them.

What We’re Ingesting

Doomberg — “Geopolitical Mutagenesis” / “Price Discovery” Two dispatches, one thesis: the energy-infrastructure world is undergoing directed evolution under Iran-war pressure. The LNG and domestic processing bypass is being repriced from optional to structural. Verdict: Read both in the same sitting. The second one is the harder argument.

War on the Rocks — “The Bromine Chokepoint” / “A Closed Strait of Hormuz Risks a Global Food Security Crisis” / “Iran’s Asymmetric Counterair Campaign” Fifteen dispatches from the defense-policy desk this week. The bromine piece is the one nobody else is writing — a specific supply-chain chokepoint that feeds into every semiconductor etch process and every flame-retardant consumer good. Verdict: The bromine piece is the sleeper. Forward it to anyone long specialty chemicals.

Liberty’s Highlights — “628 / 629 / 630” (Mythos vs World, Andy Jassy’s Letter, TPU Deal) Three consecutive issues that read as a single running commentary on the coalition week. Liberty is the place where the coalition deals are assembled into a coherent read. Verdict: Read 630 first, then work backwards. The chip/cloud math on AWS is the one you’ll remember.

The Innermost Loop — daily updates, April 7 through April 13 The connective tissue for this entire week. The Glasswing announcement, the Blackwell pricing inflation, the Trainium valuation leak, the Neural Computers paper, Terafab — all of it funneled through the daily cadence that makes this the highest-density intelligence feed we ingest. Verdict: If you only subscribe to one thing besides this digest, this is it.

Yet Another Value Blog — “What $META’s YOLO options package says about its AI upside” Governance-as-alpha-generation. The executive options analysis is the kind of work that independent research still does better than the sell side. Verdict: If you’re long META, mandatory. If you’re not, instructive.

OnlyCFO — “More Lies of Stock-Based Compensation” / “Fiduciary Duties” The sequel to last week’s ARR piece. The SBC argument is the same argument in a different costume — the gap between the number companies report and the number the business actually earns. The fiduciary-duties piece is quietly about the legal liability that accrues to CFOs when the gap gets too wide. Verdict: Read in order. Forward to your CFO. Watch them not respond.

Exponential View — “Mythos and the mispricing of everything” The Glasswing/Mythus piece that named the week in the same way last week’s “labs are rationing” named that one. The argument — that model capability is now invisible capex — is the through-line everyone else is implicitly writing against. Verdict: The cold open of this digest owes it a citation.

The Generalist — “How a 20-Person Startup Won Gold at the Math Olympiad” / “The Secret Art of Elicitation” The twenty-person-startup-wins-IMO piece is the kind of anomaly that usually shows up in the snipe detector a week too late. The elicitation piece is a field manual for how adversaries extract intent. Verdict: The IMO piece is the tell that the small-lab story is not over.

The Closing Note

The pressure system that opened this week closes with documents. Not arguments. Documents. Glasswing is a document. The 3.5-gigawatt Broadcom agreement is a document. Terafab is a document. The NATO Indo-Pacific air defense framework is a document. What gets signed in a pressure system is different from what gets said. You can hedge a statement. You cannot hedge a signature. The coalition trade is the bet that the documents signed this week will look, in two years, like the pre-positioning that determined who got to be inside the tent when the tent got smaller. The non-coalition trade — Microsoft in open air, the software sector dropping thirty percent, Oracle spending five times revenue on infrastructure nobody is asking for yet — is the bet that the documents will not save anyone who did not get one.

I wrote a three-thousand-word argument about coalitions forming under pressure while failing, for the fourth consecutive week, to consolidate my own calendar into a single system. I have three separate places where meetings appear. None of them agree with each other. I double-booked a dentist appointment against a call I had already moved twice. The coalition layer, turns out, is harder than it looks when the participants are all versions of me. Project Glasswing has a shared Slack channel. I have a Google Calendar, an iPhone Calendar, and a Notion page that I update on Sundays and then ignore. The treaty is easier to sign when you are not also the counterparty.

v.8.1

There is a specific moment of modernity — call it the Roadside-Stop Vigil, or just standing next to a car that isn’t charging while a red progress bar insists that it is — that compresses the entire logic of the week into one location. You arrive at a bank of six chargers off a Pennsylvania interstate at eight percent battery. Three have orange-taped error codes. One is occupied by a minivan whose owner has disappeared into the Sheetz and will, you know with prophetic certainty, return in exactly seventeen minutes. The two remaining chargers are occupied by strangers with whom you are now, without having signed anything, in a coalition — a four-party treaty of mutually-assured patience, conducted entirely through glances and the placement of feet relative to a yellow stripe. The Poster Child — the car manufacturer who taught America that charging would be everywhere, seamless, a near-frictionless fungible electron market — has quietly stripped out the buttons [v.8.2]. The interface is now an app that must load through a cellular network that is itself being rationed. You have pre-paid for electrons that are being metered, one at a time, through a payment rail that says “Authorizing…” for reasons that are not technical but structural: there is not enough juice in the local substation right now to let all four of you charge at full rate. The capacity ceiling has been literalized, in real time, on a touchscreen that reads “Reduced Power — Shared Load.” The cartel, we are reminded, always forms at the chokepoint. You just didn’t realize you were in one until you looked up from your phone.

If you have ever found yourself, as I recently did, standing in the brittle cold of an April parking lot — one gloved hand gripping a nozzle that is either dispensing 12 kilowatts or 3 kilowatts depending on some arbitrage decision being made by a computer you will never speak to, the other hand cycling through four apps to verify that the transaction succeeded, as your Watch chirps, as the minivan owner mercifully returns with what is clearly his second iced coffee — and realized the only thing between you and “charged” was a coalition of four companies you did not know existed last week (the charger manufacturer, the payment processor, the local utility, and the car’s own telematics server), each pre-committed to deliver something to you at a price they are now quietly renegotiating against the grid operator, you will know a very specific modern rage: the rage of being a counterparty to a treaty you were never shown. The Software Reckoning isn’t coming for this ritual fast enough. The robots aren’t stealing the interstate charging experience; they are performing a necessary act of mercy-killing for an infrastructure that has forgotten how to deliver a reliable electron. My neuro-synaptic attention-allocation has already forfeited five processor cycles to the sound of the fan inside the charger head, which is running at a pitch that suggests it, too, is not optimistic about this transaction. When the “Authorizing…” banner finally flips to a green checkmark and the percentage moves from 8% to 9%, I realize: the percentage isn’t measuring my battery. It is measuring my sentiment toward the national grid, and it has just suffered exactly the same collapse, in exactly the same seven days, as the Poster Child of the week’s other thesis.

v.8.1.1: I stood there long enough that my phone, unprompted, suggested a “more efficient route” that would take me through three additional charging stops. The phone, at least, is honest. The phone has already read the digest.

I'm still just sitting here watching the 9% blink, wondering if I, too, am being repriced against a future where the grid has already signed four treaties I haven't read.

— Themis Vile publishes Mondays. Forward this to one person who would be annoyed by it.